U.S. Market Overview

Recap of Last Week:

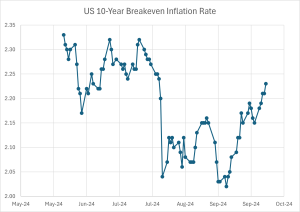

The U.S. economy posted another strong performance in September with a 254k jump in nonfarm payrolls and unemployment falling to 4.1%. This robust labor data prompted a market recalibration, reducing expectations for aggressive rate cuts by the Federal Reserve, which now points to a more moderate -54 bps by year-end. The wage growth of 0.4% further supported the view that the economy remains on solid footing, diminishing concerns about a near-term recession.

Bond markets saw significant movement, with the 10-year Treasury yield rising 13.2 bps, reflecting shifting expectations around future Fed policies. While U.S. equities faced pressure due to the likelihood of more conservative rate cuts, the overall sentiment remains cautiously optimistic.

Outlook for the Week Ahead:

- Key Data Releases:

- CPI Report (Thursday): A modest increase of 0.1% overall and 0.2% excluding food and energy is anticipated, with the headline y/y inflation expected to dip to 2.3%.

- Jobless Claims (Thursday): Insights into the labor market’s ongoing strength.

- PPI and Michigan Consumer Sentiment (Friday): Additional indicators for inflation trends and consumer outlook.

- Earnings Season Begins:

Major U.S. financial institutions, including JPMorgan, Wells Fargo, and BlackRock, will report this week. These earnings reports, combined with inflation data, are expected to drive market volatility.

source: J. Knobel Investor Services Limited / FRED

Europe Market Overview

Recap of Last Week:

In Europe, economic headwinds have shifted the focus of the European Central Bank (ECB) towards easing, as recession fears grow.

Meanwhile, China and Japan have also made policy shifts, with China’s ongoing easing in response to its economic slowdown and Japan shelving plans for another rate hike.

Outlook for the Week Ahead:

- ECB Meeting Outlook (ECB rate decision due October 17th):

Recession risks continue to loom large, and the ECB is expected to explore options for potential rate cuts. Markets will be closely watching for any hints of dovish moves. - BoE Easing Expectations:

With inflation still high but growth faltering, the BoE may reinforce signals of upcoming rate cuts in the months ahead. - Geopolitical and Commodity Pressures:

Rising geopolitical risks and potential disruptions in energy markets could add volatility, especially in European equities and commodities.

source: J. Knobel Investor Services Limited / FRED

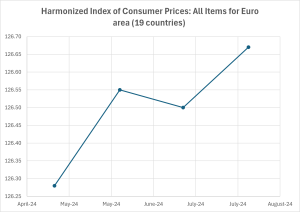

ECB Rate Outlook: The ECB may hold rates steady since Eurozone consumer prices remains elevated.

Key Market Themes for This Week:

- Diverging Central Bank Policies:

While the Fed in the U.S. may slow its rate-cutting path, the ECB and BoE are increasingly leaning towards easing. - Inflation and Labor Data in Focus:

U.S. and European markets will be guided by key inflation data this week, shaping central bank actions for the remainder of 2024. - Earnings Season Begins:

Major corporate earnings, especially from U.S. financial giants, will offer insights into how businesses are navigating economic uncertainty.

Prepared by:

John Knobel, Managing Director

J. Knobel Investor Services Limited

Office: +357 22 258 790 (Recorded line)